Picture this: you’re lying awake at 3 AM, wondering if you’ll ever have enough stashed away to actually stop working. You’re not alone. Nearly 2 in 5 Americans lose sleep over that exact fear. But here’s the thing—worrying won’t build wealth. Running the numbers will.

Whether you’re 25 and just starting or 55 and playing catch-up, understanding USA retirement savings by age benchmarks gives you a roadmap. Not some arbitrary goalpost meant to shame you. A genuine tool for clarity. The Federal Reserve’s latest Survey of Consumer Finances drops some eye-opening numbers. Let’s unpack them together. No judgment. Just math.

Quick Answer: Why Retirement Calculators Are Your Shortcut to Financial Peace

Average retirement savings for American households sits at $333,940. But the median tells a different story—just $87,000. Why the huge gap? Outliers. Billionaires and high-earners yank that average upward like a tugboat pulling a cruise ship. The median better reflects real people like you and me.

So where do you land? More importantly, how do you figure out your target number? That’s where retirement calculators enter the chat. These tools transform abstract anxiety into concrete action steps. They handle the heavy lifting so your brain focuses on strategy rather than arithmetic.

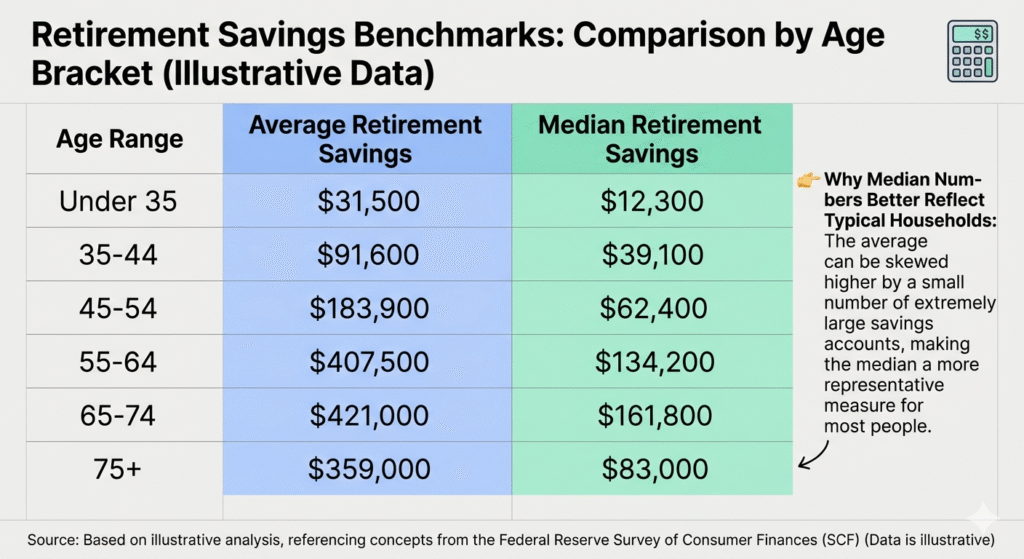

Average Retirement Savings by Age: What the 2026 Data Actually Reveals

Let’s cut straight to the Federal Reserve’s latest findings. These numbers represent real households across America. Your neighbors. Your coworkers. Maybe even you.

| Age Range | Average Retirement Savings | Median Retirement Savings |

|---|---|---|

| Under 35 | $49,130 | $18,880 |

| 35-44 | $141,520 | $45,000 |

| 45-54 | $313,220 | $115,000 |

| 55-64 | $537,560 | $185,000 |

| 65-74 | $609,230 | $200,000 |

| 75 and older | $462,410 | $130,000 |

Notice something crucial here. The averages tower over the medians. That’s because retirement savings benchmarks get skewed by the ultra-wealthy. Don’t compare your Chapter 1 to someone else’s Chapter 20.

How Much You Should Have Saved at Every Age (Plus the Formula to Find Out)

Here’s the million-dollar question—literally. How much should you actually have saved? Financial pros typically recommend stashing 10-15% of your income annually. But that’s a starting point, not gospel.

Your target depends on three variables: desired retirement age, expected lifestyle, and life expectancy. Plug those into a 401(k) calculator and suddenly the fog lifts. You see exactly what monthly contributions create which future outcomes.

For example, a 30-year-old earning $60,000 who saves 12% with a 3% employer match could hit $1.2 million by 67. That’s assuming 7% annual returns. The calculator shows the path. You just have to walk it.

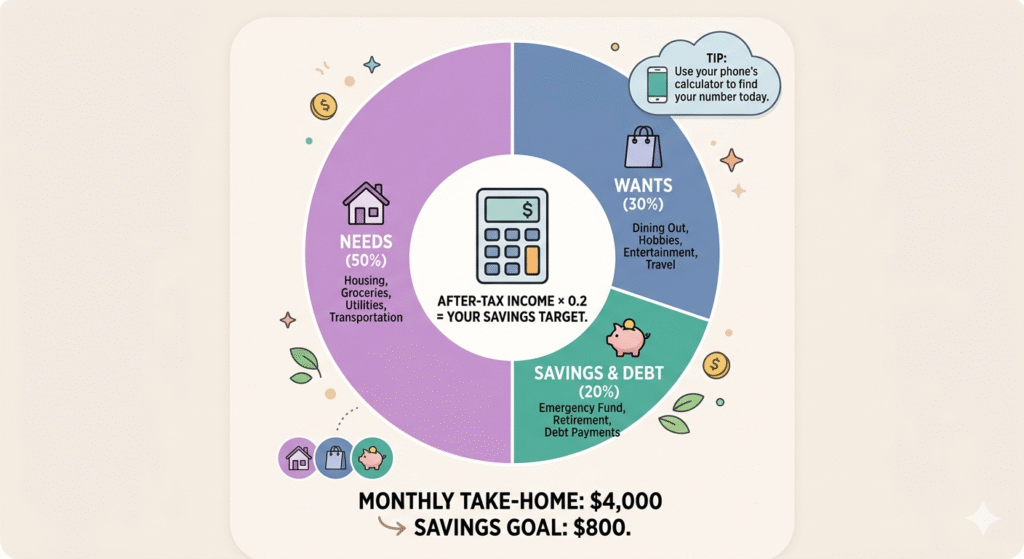

The 50/30/20 Monthly Budget: Running the Numbers That Actually Work

Remember the classic 50/30/20 rule? Fifty percent for needs, thirty for wants, twenty for savings and debt. It’s simple. It’s elegant. And it works—if you actually track it.

Grab your phone’s calculator app right now. Add up your after-tax monthly income. Multiply by 0.2. That’s your target savings rate by age bracket. For a $4,000 monthly take-home, you’d aim for $800 into retirement accounts, emergency funds, and debt payoff.

But here’s where most people stumble. They guess. They estimate. They round down. Use actual numbers pulled from bank statements. Data doesn’t lie. Your memory does.

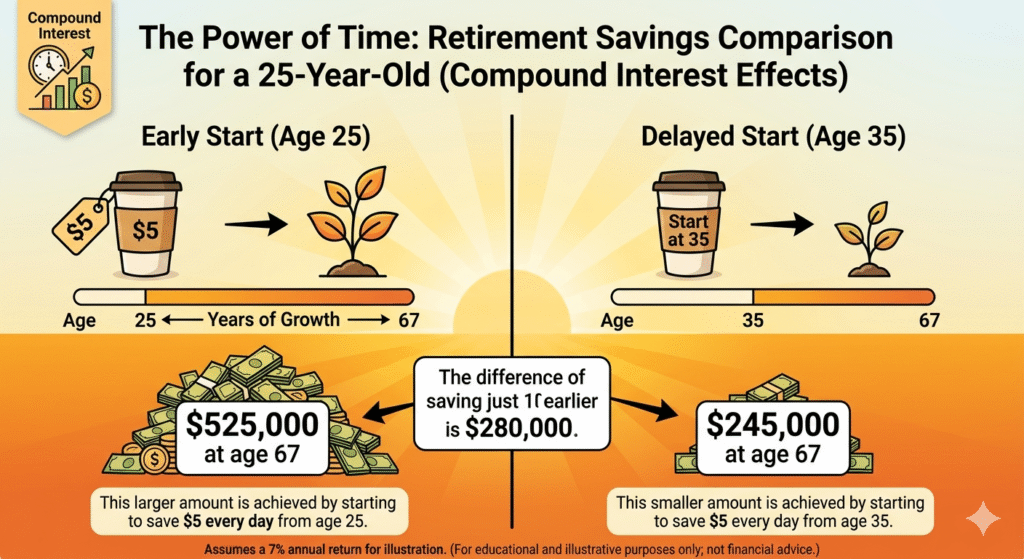

Savings Goals in Your 20s: Small Numbers, Big Compound Growth

Your twenties feel like financial amateur hour. Low salaries. Student loans. Rent that eats half your paycheck. Yet this decade holds superpowers you’ll never get back: time and compound interest.

A 25-year-old who saves just $200 monthly with a 7% return accumulates nearly $525,000 by 67. Wait until 35 to start? That same $200 monthly becomes barely $245,000. The difference? About 280 grand. For doing absolutely nothing different except starting earlier.

Compound interest calculators reveal this magic instantly. They show you that skipping one daily latte funds your future freedom. Not through deprivation. Through awareness.

Savings Goals in Your 30s: Catching Up Without Burning Out

Welcome to the squeeze decade. Childcare costs. Mortgage payments. Career advancement pressure. Your twenties were practice. Your thirties are the real game.

About 62% of households in this age bracket hold retirement accounts. The median sits at $45,000. If you’re above that? Great. Below? Also fine—because you’re reading this now.

Use a Roth IRA calculator to see how after-tax contributions grow tax-free forever. Max it out at $7,000 annually (2026 limits) and you’ve parked over half a million dollars by retirement. That’s assuming you start at 35. Your future self will high-five you.

Savings Goals in Your 40s: Accelerating with Precision

Peak earning years typically hit during your forties. Your income rises. Your expenses maybe stabilize. This is your moment to punch the accelerator.

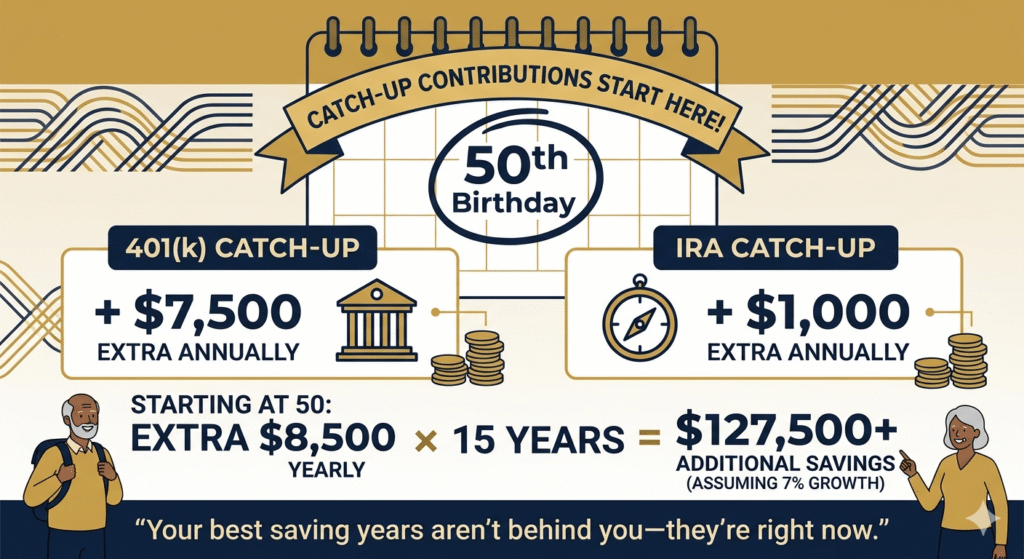

The median retirement savings by age 45-54 hits $115,000. But remember—median means half have more, half have less. Wherever you land, consider catch-up contributions if you’re 50 or older. The IRS allows extra $7,500 in 401(k) contributions starting at 50.

Run your numbers through a retirement readiness calculator. It factors in your current savings, expected Social Security, and desired lifestyle. Then it tells you exactly how much extra to stash monthly. No guesswork. Just math.

Savings Goals in Your 50s and Beyond: The Final Stretch

The finish line comes into focus during your fifties. About 57% of households aged 55-64 hold retirement accounts. Median savings: $185,000. Average: $537,560. Notice the gap again? Don’t stress about averages. Focus on your personal finish line.

This decade demands precision. Use a required minimum distribution calculator to estimate what you’ll need to withdraw starting at 73. Plan your Social Security claiming strategy carefully. Delaying benefits until 70 increases your monthly checks by roughly 8% annually.

And please—run a retirement withdrawal calculator before tapping accounts. One wrong move early can cascade into shortfalls later.

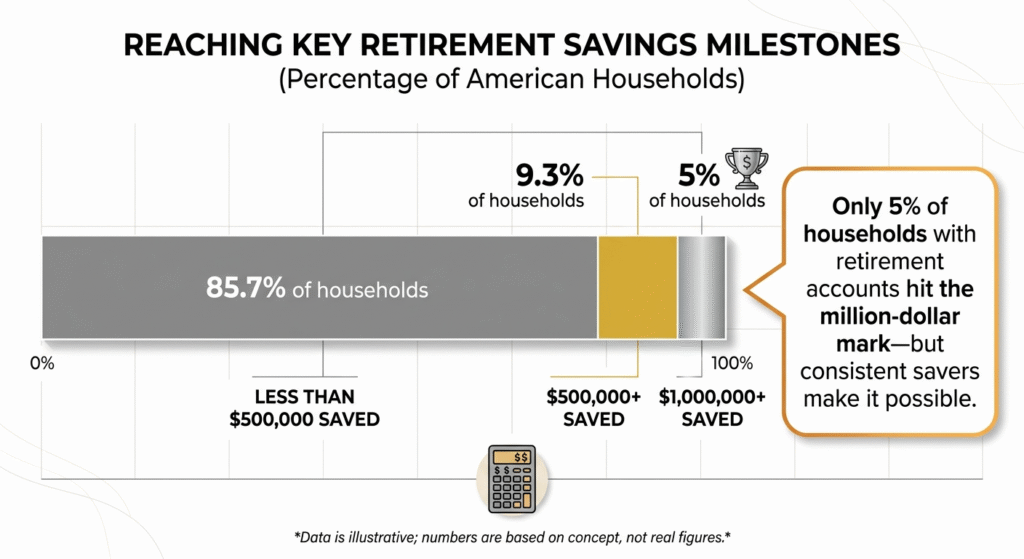

How Many Americans Have $500K or $1M Saved? (And What They Did Differently)

Curious about the million-dollar club? Only about 5% of households with retirement accounts hit the $1 million mark. For $500,000, roughly 9.3% qualify. These aren’t lottery winners or tech IPO millionaires. They’re consistent savers who leveraged time and compound growth.

What did they do differently? They calculated early and often. They used average retirement savings data as motivation, not intimidation. They automated contributions. They increased savings with every raise. They checked progress annually and adjusted course when needed.

Sound complicated? It’s not. It’s just math with a dash of discipline.

Where to Keep Your Savings: High-Yield Accounts vs. Investment Calculators

Parking retirement money requires strategy, not just effort. High-yield savings accounts currently offer 4-5% APY—great for emergency funds and short-term goals. But for retirement? You’ll likely need stock market exposure to outpace inflation.

Use an investment calculator to compare scenarios. A $50,000 lump sum growing at 4% (high-yield savings) becomes about $110,000 in 20 years. At 7% (diversified portfolio), it hits roughly $193,000. That difference funds years of retirement.

But here’s the catch: markets fluctuate. A compound interest calculator shows average returns, not guaranteed ones. Diversify. Stay consistent. Don’t panic-sell during downturns.

How to Increase Your Savings Rate: 5 Calculator-Based Strategies That Work

1. The Unit Price Habit

Check price per ounce at grocery stores. That “bulk” deal often costs more. Savings add up fast.

2. The Time Audit

Multiply daily habits by 365. Thirty minutes scrolling becomes 182 hours yearly. Redirect that time toward side income or skill-building.

3. The “Pause and Punch” Rule

Before any non-essential purchase over $50, subtract it from your balance. Seeing the new total prevents impulse spending.

4. The Cost Per Use Calculation

Divide purchase price by expected uses. A $200 coat worn 100 times ($2/use) beats a $40 coat worn 5 times ($8/use).

5. The 1% Rule

Increase retirement contributions by 1% annually. You won’t miss the money. Your future self absolutely will.

The Bottom Line: Your Retirement Journey Starts with One Calculation

Here’s what I want you to take away. USA retirement savings by age data provides context, not verdicts. You’re not behind. You’re not ahead. You’re exactly where you are—and that’s perfectly positioned to start.

Grab a calculator today. Any calculator. Your phone works fine. Run your numbers through one of the tools mentioned above. See where you stand. Then make one small adjustment. Increase contributions by 1%. Switch to a high-yield account. Automate something you’ve been guessing about.

The most powerful financial tool isn’t a spreadsheet or an app. It’s your decision to start. Today.

Join the Conversation!

What age bracket are you in? Have you checked your retirement savings benchmarks lately? Drop a comment below—I’d love to hear your story. And if you found this helpful, share it with a friend who needs to see those numbers too.

Leave a Reply